Executive Summary

Gross-to-Net (GTN) is one of the most underestimated risks in generic pharmaceutical finance.

For emerging and mid-market generics companies, the question is rarely whether GTN matters ; it is when complexity crosses the line from manageable to material.

Oracle NetSuite is often positioned as either a complete GTN solution or entirely insufficient. Both views are wrong.

Archer Insights’ point of view is simple:

- NetSuite is an excellent financial foundation for Gross-to-Net

- It is not a purpose-built GTN calculation engine

- The winning strategy is phased, audit-first, and scale-aware

When implemented correctly, NetSuite can:

- Support GTN accruals and controls

- Serve as the system of record for revenue and liabilities

- Provide a clean audit trail under ASC 606

As GTN complexity grows, NetSuite should not be replaced ; it should be paired with a specialized GTN platform such as Model N or Revitas.

Archer helps generics companies design this journey deliberately, avoiding over-engineering early and rework later.

1. What Makes GTN Hard in Generics

This section intentionally focuses on operational reality, not theory.

GTN complexity in generics is driven by:

- Chargebacks (high volume, contract-driven, retrospective)

- Government programs (Medicaid, Medicare Part D, 340B)

- Channel mix volatility (wholesalers, specialty, direct)

- Time lag between shipment, claim, and settlement

- Auditor scrutiny under ASC 606

Any system supporting GTN must handle:

- Accrual estimation at time of sale

- Claim validation and reconciliation

- Periodic true-ups

- Transparent assumptions and controls

2. When NetSuite Is a Good Fit for GTN

NetSuite is a good fit when GTN complexity is real but still manageable.

Typical Company Profile

-

Early to mid-stage generics company

-

Limited product portfolio (generally < 20 SKUs)

-

Primary distribution through 1–3 wholesalers

-

Contract structures are relatively stable

-

Government exposure exists but is not dominant

-

Finance team is hands-on and process-driven

GTN Characteristics

- Chargebacks are material but not overwhelming in volume

- Accruals can be estimated using historical percentages

- Rebates and returns are predictable

- Quarterly true-ups are acceptable

Why NetSuite Works Here

In this scenario, NetSuite can:

- Act as the system of record for revenue and accruals

- Provide clean audit trails and SOX-aligned controls

- Support GTN via:

- Custom accrual logic

- Contract and pricing masters

- Chargeback validation workflows

- Period-end true-up journal entries

The key is that GTN is engineered as a process, not expected to be “native.”

3. NetSuite’s Role When It Is a Good Fit

When NetSuite is a good fit, it typically plays three critical roles:

1. Financial System of Record

- Books gross revenue

- Holds GTN accrual liabilities

- Posts adjustments and true-ups

- Supports multi-book (GAAP vs management)

2. GTN Accrual & Control Framework

- Accruals calculated at shipment or invoicing

- Assumptions stored and version-controlled

- Clear linkage between sales, accruals, and settlements

3. Audit & Compliance Backbone

- Documented GTN methodology

- Repeatable month-end process

- Strong traceability from estimate → actual

In this model, NetSuite is not trying to outsmart GTN. It is enforcing discipline, consistency, and financial integrity.

4. When NetSuite Is Not As Good A Fit As The GTN Engine

NetSuite alone becomes insufficient when GTN complexity outpaces percentage-based estimation.

Typical Company Profile

- Mid-to-large generics manufacturer

- Large SKU count with frequent launches

- Heavy Medicaid, Medicare Part D, and 340B exposure

- Multiple GPO, PBM, and government contracts

- High chargeback claim volumes

- Aggressive pricing changes

GTN Characteristics

- Accrual accuracy materially impacts earnings

- Chargebacks are contract-specific and claim-driven

- Government programs require statutory logic

- Forecasting and analytics are critical

- Auditors expect system-level controls

In this environment, GTN is no longer just accounting ; it is a core commercial operation.

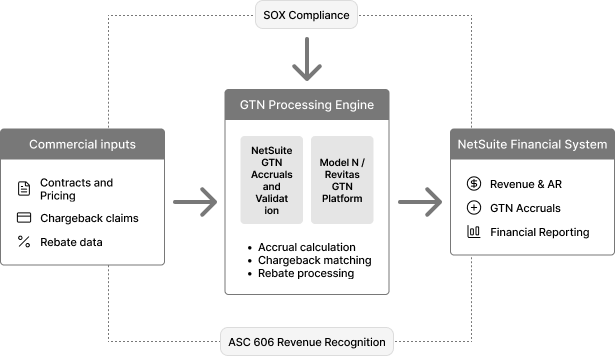

5. NetSuite’s Role When It Is Not the GTN Engine

Even when NetSuite is not the GTN calculation engine, it still plays a central role.

NetSuite as the Financial Anchor

- Remains the general ledger and AR/AP system

- Receives summarized GTN results from a GTN platform

- Maintains statutory and management reporting

GTN System as the Calculation Engine

- Specialized GTN platforms handle:

- Chargeback adjudication

- Medicaid and 340B logic

- Contract price validation

- Forecasting and scenario modeling

Integration Model

- GTN system calculates detailed deductions

- NetSuite preserves audit traceability

- NetSuite posts:

- Accruals

- Settlements

- Adjustments

In this model, NetSuite governs the money, while the GTN platform governs the math.

6. Common Mistakes to Avoid

- Expecting NetSuite to be a plug-and-play GTN solution

- Overbuilding GTN logic too early

- Underestimating audit expectations

- Treating GTN as a one-time implementation

- Letting GTN calculations live outside controlled systems (spreadsheets)

7. Practical Decision Framework

| Question | If “Yes” | If “No” |

|---|---|---|

| Is GTN manageable with estimates? | NetSuite-led GTN | Dedicated GTN platform |

| Is government exposure limited? | NetSuite viable | NetSuite + GTN system |

| Are auditors comfortable with process-based controls? | NetSuite works | Specialized tooling needed |

| Is SKU/contract growth expected soon? | Stage NetSuite first | Plan GTN integration early |

8. What Companies need to be aware of

- NetSuite is a strong foundation for Gross-to-Net ; not a silver bullet

- GTN success depends on controls, assumptions, and audit defensibility

- The smartest approach is phased: NetSuite first, specialized GTN tooling later

- Archer’s role is to design, implement, and govern this evolution end to end

The smartest approach is often phased: start with NetSuite-led GTN, then integrate a specialized GTN platform as scale and exposure demand it.

9. Archer Insights Point of View and Positioning

Archer Insights approaches Gross-to-Net not as a software configuration exercise, but as a commercial-to-finance operating model problem.

Most GTN failures do not come from the math. They come from:

- Poor contract structure

- Weak linkage between commercial strategy and finance

- Accrual logic that auditors cannot follow

- Over-engineering too early or under-engineering too late

Archer’s positioning is intentionally pragmatic:

- NetSuite first, but not NetSuite forever

- Design GTN as a scalable control framework

- De-risk future GTN platform adoption

Archer’s GTN Philosophy

Archer believes:

- NetSuite should always be the financial system of record

- GTN logic should mature in phases

- Specialized GTN platforms should be added only when economic and audit risk justify it

This avoids the two most common mistakes in generics:

- Implementing a heavy GTN platform too early

- Letting GTN live in spreadsheets for too long

Archer’s Phased GTN Roadmap

Phase 1: NetSuite-Led GTN Foundation

- GTN accrual framework inside NetSuite

- Contract and pricing master design

- Chargeback intake and validation workflows

- SOX- and audit-ready documentation

Phase 2: Hybrid GTN Model

- Introduce Model N or Revitas for calculation complexity (Archer does not sell this)

- NetSuite remains the GL and control layer

- Clear ownership split between systems

Phase 3: Scaled GTN Operations

- GTN platform becomes calculation engine

- NetSuite becomes the financial authority

- Archer governs integration, controls, and audit alignment

10. NetSuite vs Model N / Revitas Responsibility Split

The table below reflects Archer’s recommended system-of-responsibility model, not marketing claims.

| GTN Function | NetSuite Responsibility | Model N / Revitas Responsibility |

|---|---|---|

| Gross revenue recognition | System of record | Not applicable |

| GTN accrual posting | Yes (GL impact) | Provides calculated values |

| Contract master (financial view) | Yes | Sync / reference |

| Contract adjudication logic | Limited | Primary engine |

| Chargeback validation | Basic / workflow | Advanced rules & validation |

| Medicaid rebate calculation | Not native | Primary engine |

| Medicare Part D logic | Not native | Primary engine |

| 340B pricing & eligibility | Not native | Primary engine |

| Forecasting & scenario modeling | Limited | Advanced analytics |

| Period-end true-ups | Yes | Provides supporting detail |

| Audit trail & SOX controls | Primary owner | Supporting detail |

| Cash application & settlement | Yes | Feeds settlement data |

11. How Archer Typically Positions This with Clients

We position the conversation around:

- Risk (earnings volatility, audit exposure)

- Timing (when complexity actually hits)

- Control (who owns the numbers)

Our typical guidance:

- If GTN errors are annoying, NetSuite-led GTN is sufficient

- If GTN errors are material, a GTN platform is justified

- In all cases, NetSuite remains the financial backbone

This keeps CFOs, auditors, and commercial leaders aligned, and avoids rework.

12. Key Implementation Takeaways

- NetSuite is an excellent foundation for Gross-to-Net

- It should never be treated as a silver bullet

- The winning strategy is phased, intentional, and audit-first

Archer’s role is to:

- Design the GTN operating model

- Implement NetSuite to support it

- Integrate GTN platforms when and only when they are justified

Appendix: Questions Auditors Will Ask (and How Archer Designs for Them)

1. How are GTN accrual percentages determined?

Expectation: Historical data, documented methodology, periodic review.

2. How do you validate chargebacks against contracts?

Expectation: System-based validation, not spreadsheets.

3. How do you ensure completeness of GTN liabilities?

Expectation: Controls tying shipments to accruals.

4. How are estimates trued up to actuals?

Expectation: Consistent, period-based true-up process.

5. Who owns GTN assumptions and approvals?

Expectation: Clear ownership and version control.

6. What happens when contracts or pricing change mid-period?

Expectation: Controlled updates with documented impact.

7. How does the GTN system integrate with the GL?

Expectation: Clear system-of-record definition.

8. Can you trace a dollar from gross sale to net revenue?

Expectation: End-to-end traceability.

9. How do you prevent management override of GTN estimates?

Expectation: Controls, approvals, and audit logs.

10. How does your GTN approach scale as volume grows?

Expectation: Roadmap, not heroics.